How the Grid Is Organized

The North American bulk power system is divided into three major interconnections, each operating as a synchronized AC network. Within these interconnections, regional organizations manage reliability and markets.

Learning Objectives

- Describe the three major North American interconnections and their significance

- Explain why the grid is organized into interconnections and balancing authorities

- Identify the role of AC synchronization and DC ties in grid architecture

Eastern Interconnection

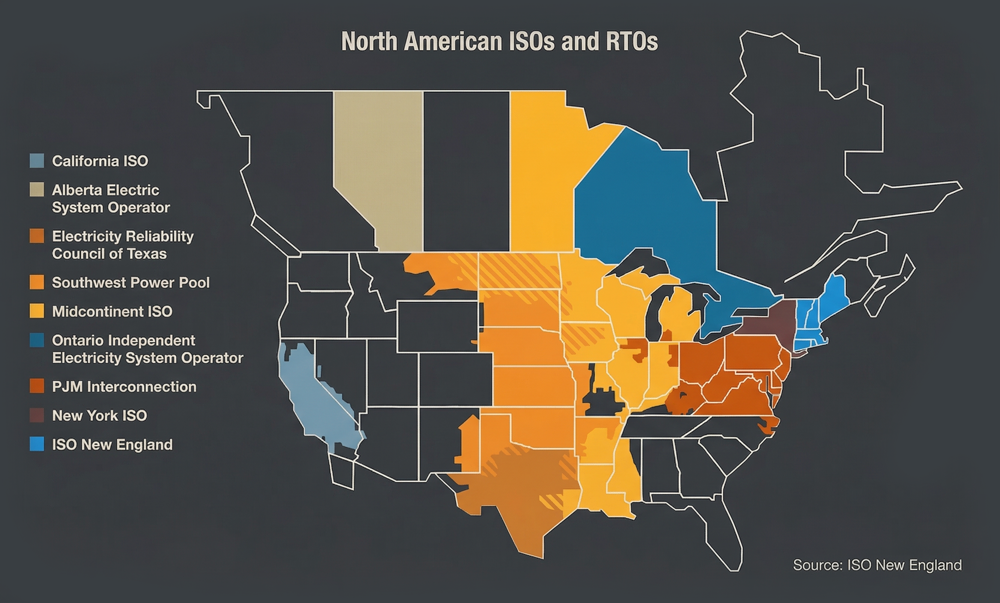

The largest, covering everything east of the Rockies (except Texas). Includes PJM, MISO, SPP, NYISO, ISO-NE, and the Southeast. All generators synchronized at 60 Hz.

Western Interconnection

Covers the western U.S. and parts of Canada/Mexico. Managed by WECC. Includes CAISO and a patchwork of balancing authorities. Connected to the Eastern via limited DC ties.

Texas (ERCOT)

Operates its own interconnection, largely avoiding federal jurisdiction. Managed by ERCOT. Connected to the Eastern by limited DC ties. Serves about 26 million customers.

NERC Reliability Regions

NERC oversees six Regional Entities (EROs) that monitor compliance with reliability standards across North America.

U.S. Electricity Market Coverage

Approximately two-thirds of U.S. electricity consumers are served within organized RTO/ISO wholesale markets.

| NERC Region | Coverage Area | Key RTOs/ISOs |

|---|---|---|

| NPCC | Northeast U.S. & Canada | NYISO, ISO-NE |

| RF | Mid-Atlantic, Great Lakes | PJM |

| SERC | Southeast U.S. | No organized market (bilateral) |

| MRO | Midwest, Great Plains | MISO, SPP |

| TRE | Texas | ERCOT |

| WECC | Western U.S., Canada, Mexico | CAISO |

Key Takeaways

- North America operates as three synchronized AC interconnections (Eastern, Western, ERCOT) linked by DC ties

- Within each interconnection, balancing authorities and RTOs coordinate generation and load in real time

- This physical architecture shapes which markets a utility can access and how power flows

Next: Who runs these markets? RTOs and ISOs — the institutions at the center of wholesale electricity.